Future challenges for the Asian refining industry – Feedback from ARTC in Jakarta 29-30 March 2017

On 29-30 March 2017 the World Refining Association gathered over 200 executives from oil industry, government/non-government bodies and other service providers at the 20th ARTC (Asian Refining and Technology Conference) in Jakarta, Indonesia for a two-day networking and information exchange. The purpose of the event was to highlight issues refining companies will face in the future, support the delegates in developing potential action plans and strategies, and prepare companies for the rocky ride ahead.

At the conference, the Asian Clean Fuels Association also presented on the issue of high quality, clean octane shortage that the Asian refining sector will face, given the trend of Asian countries improving their fuel standards.

We are looking at a significant amount of projects to build new refining capacity and to upgrade existing infrastructure in Asia which is very much needed as demand for refined products keeps outpacing supply till date. However, the ambitious schedules in the region are hampered by financing obstacles as the search for JV partners proves difficult in the current low crude price environment. A number of projects have already been delayed (most recently in Vietnam and Indonesia) and further postponements may occur as technical and environmental challenges are mounting.

Conference programme

The two-day programme touched on a wide range of topics and issues for the refining industry – we dare to summarize the event into four blocks:

Refining development and future in Indonesia and the rest of Asia

Margin concerns versus technical innovations and requirements

Utilization and performance enhancements throughout the entire supply chain

Interdependence between the refining and petrochemical industry

Challenges for the refining industry

Apart from the a.m. supply & demand issue, any oil company around the globe is looking at

Low crude oil price environment medium-term which still carries the full volatility risk

Increasingly tougher regulations and requirements which add on to the production cost burden

… while the margin outlook is expected to stay range-bound

… and competition from new and alternative supply sources grows

Global crude oil output keeps generating an oversupply situation and apart from the current OPEC’s/non-OPEC’s output cut agreement we can see other countries making strategic plans on limiting future supply further. China has already announced to cut crude supplies by 2020 to a targeted 200m MT/y, compared to a level of 214m MT in 2015 which equates to a 6.5% reduction in order to boost the domestic market for Natural Gas. Natural Gas consumption is predicted to grow by 8.9% p.a. to reach 207m cbm by 2020.

We can also see different and incoherent energy strategies being developed by individual countries, with countries like Germany and Japan developing long-range plans for hydrogen projects. Oil majors such as Shell and ExxonMobil are developing future fuel strategies in which LNG/Natural Gas play a pivotal role.

EV technologies are being promoted for the main automotive fuel markets in the US, Europe but also in China and Japan, while alternative fuels like biofuels keep being mandated in some parts of the world, all leading to a potentially reduced demand for conventional, refined fuels.

Main conference topics

In total, thirty-seven papers were presented during the two-day event, covering a wide range of topics related to the future challenges for the refining industry. The scope entailed

Hydrogen technology developments and alternatives

Nuclear energy options

Strategies and global solutions such as hydro-cracking to improve competiveness

Desulphurization issues and solutions for the marine fuel and road transportation market segment

Proposed technologies to meet Benzene and Sulphur restriction challenges in petrol

Value-chain increases for petrochemicals

Focus in most papers was on generating “value from the bottom barrel” by observing capital investment and cost-reduction objectives, and to utilize cheaper feeds and supply higher value markets.

Highlights of the conference

Over the next few pages we will share some of the main discussion topics from the conference which we have extracted from the papers presented:

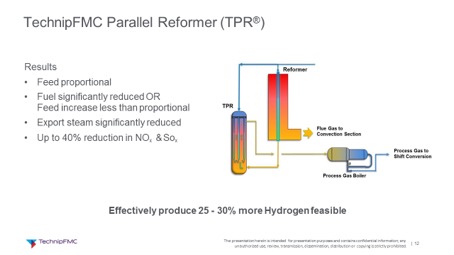

Adapting the Hydrogen Plant to Changing Environments - TechnipFMC

Hydrogen plant modernization appears to be a viable and attractive option, compared to building new plants. A plant upgrade is meant to come at a lower overall cost and requires a lower schedule. Additionally, less investment in new equipment items is needed.

Capacity increases are feasible for up to 30-40% of initial nameplate capacity and can eventually be combined with other objectives for further plant modernization.

The chart underneath shows TechnipFMC’s Parallel Reformer process as an example for possible hydrogen production increases:

(Chart 1)

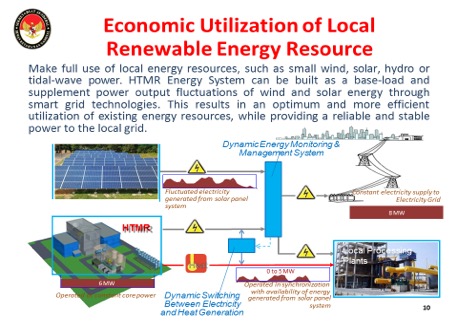

Nuclear Energy Option for Indonesian Economic Development – National Resilience Council of Indonesia

HTMR (high-temperature modular reactor), a generation IV nuclear reactor-based, small energy distributing system, designed for areas without large electricity grid, could be implemented in Indonesia’s Timur region in order to overcome the lack of electricity and portable water availability in the region.

(Chart 2)

HTMR units are small plants in comparison to i.e. Diesel generators and they are very flexible in terms of capacity increase requirements. The generation IV model is categorized as “super safe” and environmentally clean. Its simple design makes it easy to operate and co-generating heat energy comes as an extra advantage.

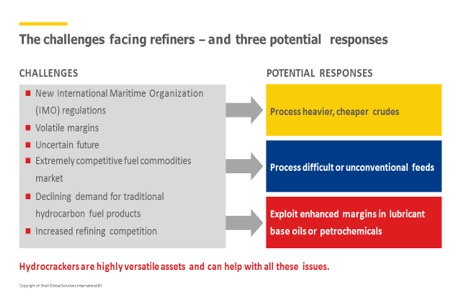

Next-level hydrocracking: Unlocking high performance in today’s turbulent markets - Shell Global Solutions

John Baric, Hydrocracking Licensing Business Manager of Shell Global Solutions, presented a paper on next-level hydrocracking as a proposed solution to today’s challenges. The chart underneath shows some of Shells’ suggested solutions to the demands:

(Chart 3)

Companies like Shell are processing heavier, cheaper crudes or non-standards feeds. They are optimizing the product slate and producing higher-value products.

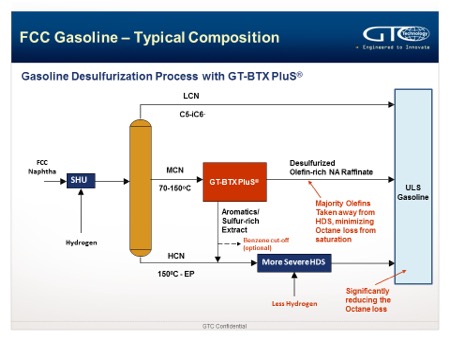

GT-BTX PluS®: Technology for FCC Gasoline – GTC Technology

A very interesting paper was submitted by Charlie Chou, Global Licensing Manager at GTC Technology. The presentation explained the possibility to de-sulphurize FCC gasoline to < 10ppm and to reduce the Benzene contents to < 0.5%, without losing as good as no octane in the process.

(Chart 4)

According to our understanding, the GT-BTX PluS process yields a Sulphur removal rate of >99% and a reduced hydrogen consumption of 60%, while the RON (octane) loss is reduced by 85%. The cost of production remains unchanged (heat consumption up, H2 consumption down).

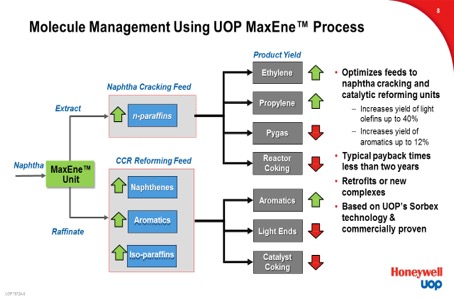

Maximize Profitability of Refining and Petrochemical Complexes by Integration and Innovation – Honeywell UOP

Dr. Gregory Funk, Senior Product Line Manager at UOP shared his views on how to maximize profitability and product output in an oil refinery by optimizing the supply into the petrochemical markets. The chart underneath shows the molecule management in UOP’s MaxEne process:

(Chart 5)

Conclusion

The WRA conference was packed with high-quality presentations and we can only extract a very small portion of the topics being discussed. The charts used above are only meant to attract your interest in some of the topics and we recommend to seek more details from the individual presenters, quoted in our newsletter as well as from others we did not make any specific reference to.

Refiners will go through a phase of immense challenges and changes over the next few years and it will be important to keep dialogues and other communication challenges open in order to obtain a comprehensive overview of all aspects of changes and keep all channels viable. The Asian Clean Fuels Association is proud to be a member of the Advisory Board of ARTC and we are looking forward to contributing technical and environmental know-how to the conference members.

In this issue of our “In Conversation with” we talked to Mr. Jeff Hove, acting Vice President and Executive Director at the Fuels Institute. In recent years we have seen some initiatives to consider policies to ban the sale of vehicles equipped with internal combustion engines (ICE), predominantly emerging in Europe, but also spreading out in parts of Asia.

In this issue of our “In Conversation with” we talked to Dr Tilak Doshi, an energy sector consultant based in Singapore. Dr Doshi shared his views and observations about the global “2050 decarbonisation” plan and move towards Electric Vehicles (EVs) with us. We would like to thank Dr Doshi for his efforts to comprehensively answer our questions which provide some highly valuable and very interesting insights into this matter, highlighting a range of topics often overlooked in the political discussion between the various stakeholders in the race to save the world from impending climate catastrophe.

In this issue of our “In Conversation with” we talked to Dr Sanjay C Kuttan, Chairman of the Sustainable Infrastructure Committee at Sustainable Energy Association of Singapore (SEAS).

.svg)

.svg)