Global octane and fuel quality trends 2019/2020 and beyond

Introduction

In this issue of our In Focus newsletter, ACFA would like to share some observations about gasoline quality and octane requirement changes perceived in the global markets in the recent past and what those changes entail for the future of the fuel-ethers markets. Our observations are intended to highlight the current developments, while our opinion expressed is meant to encourage some thought process among our readers.

After the European Union has managed to establish itself as a premium grade (RON95) market a number of years back, when Regular gasoline disappeared from service stations almost completely, large parts of Asia, the Middle East and Africa are yet far from achieving similar standards, albeit gasoline quality changes and octane ratings have been identified and addressed as a pivotal factor to tackle air pollution problems as well as increasing fuel efficiency ratings. In the US and in Canada consumer trends are also indicating a shift to higher quality and octane types in recent years. Similar to parts of Asia, Latin America has plenty of space left for further improvements, while consumer cost for transportation fuels plays an important role and environmental awareness is less developed. This obviously applies even more so to Africa where fuel quality standards are till date not on every consumer’s mind and hence often neglected by politicians and legislators. Another interesting region is North-East Asia where fuel quality today is largely at world-leading standards, while octane requirements, i.e. in China and Japan, fall short of other developed markets in the world.

Apart from the positive octane improvement trend observed in many countries, ACFA also noticed that higher octane gasoline grades, such as SuperPlus, have failed to leave a big impression on most markets, maintaining a market share in single-digit territory. This we believe is due to the higher price of the product and the lack of wide-spread knowledge among consumers about the benefits of those gasoline grades. Some oil companies identified SuperPlus as a possibility to polish the company image and capture a niche market share but efforts retreated when advances were seen as minimal and against the company’s overall position on octane. The strongest proponent of high-octane fuel standards is in fact the automotive industry which released the 2019 edition of the Worldwide Fuel Charter in October 2019. This sixth edition of the WWFC introduces a new Category 6 gasoline quality to address anticipated vehicle and engine regulations for emission control and fuel efficiency in certain major markets, recommending octane standards of RON98 and RON102. On the legislative side, focus has shifted towards emission reduction and alternative energy developments, as long-term targets for 2030 and beyond.

Reference above-made points, higher-octane gasoline comes at a price for the producer and the challenge is to recover this in the end use market. Based average price spreads in Europe and in Asia, margins achieved for the higher octane grade are usually lower than the margins achieved for the standard grade. The main cost factor for the producer is that the octane gap between the available base blend and the target blend needs to be made up by the intake of octane boosters. In today’s environment, this confines the choice to oxygenates (fuel-Ethers, Ethanol) and a limited number of other components, given the prevailing gasoline specifications.

Looking at the different trends and developments by region we see the following picture unfolding in the three potentially biggest growth areas for octane globally:

South-East Asia

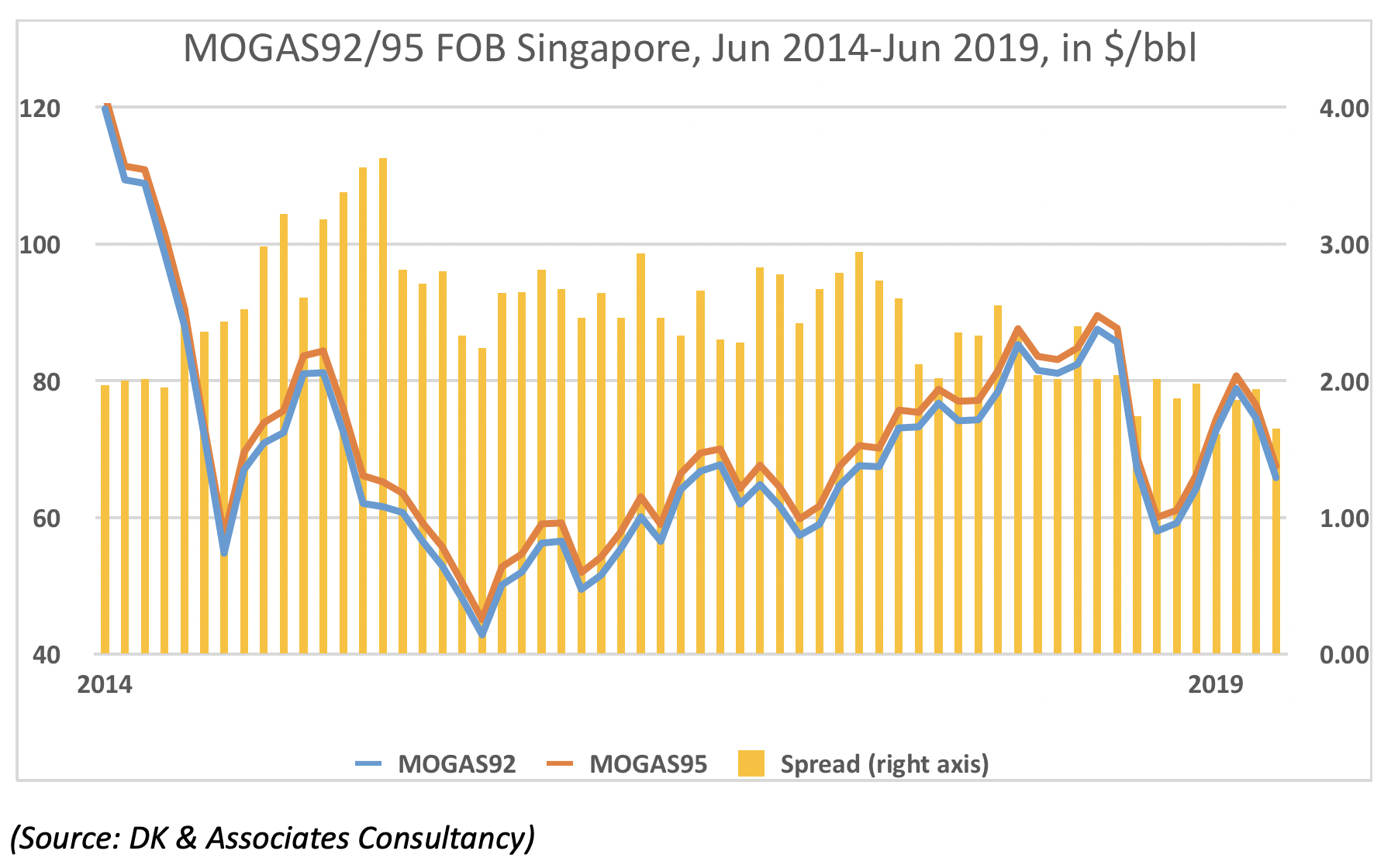

During the last decade the region’s octane demand increased significantly, caused by a range of specification changes in South-East Asia itself but also due to the impact from markets outside the region, usually supplied with fuel produced locally in i.e. Singapore, Thailand and India. Octane requirements started to grow before the refining industry was ready to reply. The shortage of refining capacity in South-East Asia was an already apparent problem when consumption began to increase over-proportionally, while the quality/(= octane) problem came in addition. During this time, markets saw the value of octane increasing sharply (here expressed as the price difference between MOGAS92 and MOGAS95, basis FOB Singapore), from on average 2 $/bbl during the first half of the decade to about 3.20 $/bbl on average during 2015. However since, the price spread has been steadily declining again, apart from some months during which market-specifics broke the trend.

A long list of refining capacity increase and upgrade projects were already announced, as the oil industry predicted the above-described developments a long time before this started to happen, and, as quality and quantity output improved, price spreads between the main gasoline grades contracted again. The above chart shows the price spread between MOGAS92 and MOGAS95, the two main gasoline grades traded in Singapore. The Singapore market was double-hit by volume and quality supply increases, due to the investment projects in South-East Asia but also elsewhere, like in China which has become Singapore’s major gasoline supplier.

While there are more new refining projects expected to increase the volume and quality supply over the next few years, we also see demand increasing, for volume at least over the next five years, and in terms of quality and octane, also beyond 2025. Fuel-ethers will play an integral part in this development, enabling refiners to comply with any potential new requirements. Underneath the reader will find a table, showing the current gasoline octane mix by main countries in Asia and a possible future scenario, based on today’s known initiatives:

Country

2020

Octane mix -market share

2025 & beyond

Octane mix -market share

Comments

China

89 / 92/ 95 / 98

15%/40%/40%/5%

92 / 95 / 98

40%/50%/10%

While China has the highest gasoline quality standards, current octane ratings are well below EU standards, leaves plenty of space for improvements

South Korea

91 & 94 / 99

>95% / <5%

91 & 94 / 99

93 %/ 7%

Very mature market, currently at Euro 5 equivalent standard, no legislative changes expected

Japan

90 / 99

92%/ 8%

95 / 98

85%/15%

Declining demand, Euro 6 equivalent standards but “low-octane” market (consumer cost awareness), requires fuel standard review, considered unlikely

Taiwan

92/ 95 & 98

20% / 80%

92 / 95 & 98

10%/ 90%

Mature market, running on Euro 5/6 equivalent standards, (% and higher RON grades represent 80%, could move towards 95 min.

Indonesia

88,90,92/ 95/ 98

>80% />17%/2%

92 / 95 / 98

80 / 15 / 5

Upgrading fuel standards to Euro 4 and phasing out 88 and 90 RON gasoline, leading to a substantial increase in octane demand

Malaysia

95 / 97 / 98

85%/ 14%/ 1%

95 / 97 / 98

90%/ 9%/ 1%

Upgrading fuel standards to Euro 5M (Euro 5 equivalent) by 2024

Thailand

91 & 95 / 97

>95% / <5%

91 & 95 / 97

>95% / <5%

Euro 4/5 equivalent standards, Ethanol gasoline represents over 90% of market, 91 RON phase-out possible but not planned

Vietnam

92/ 95

40% / 60%

92/ 95

40% / 60%

Euro 4 gasoline standards, Euro 5 planned for 2022, octane mix unlikely to change

Philippines

91 / 95 / 97

80%/15%/ 5%

91 / 95/ 97

80%/15%/ 5%

Euro 4 fuel standards, all gasoline grades come as E10, no change to octane ratings expected short-to-medium term

India

91 / 95/ 98

96%/ 3% / <1%

91 / 95/ 98

90%/10%/<1%

India currently transitioning from Bharat 4 (Euro 4) to Bharat 6 (Euro 6) fuel standards,

95 RON market share expected to grow to >10% on consumer preference

Australia

91 /95 & 98

70%/30%

91 /95 & 98

70%/30%

Weak gasoline standards (Euro 3/4) are being maintained till 2027, high Sulphur, high aromatics contents, unlikely to see the country making an effort on octane

The green-shaded countries in the table above represent the highest potential for octane advances in the future, may it be on consumer behaviour or by fuel standard reviews and new requirements. The selection coincides with the by far biggest gasoline consuming nations in Asia, having the top three: China, Indonesia and India included in the selection. With China and India are at best possible levels in terms of fuel quality standards, the high-octane proponents can now focus on enhancing the compression ratio of the fuels. In Indonesia which is in desperate need of higher fuel quality standards, the efforts to increase quality should go hand-in-hand with the push for a higher octane rating.

Middle East

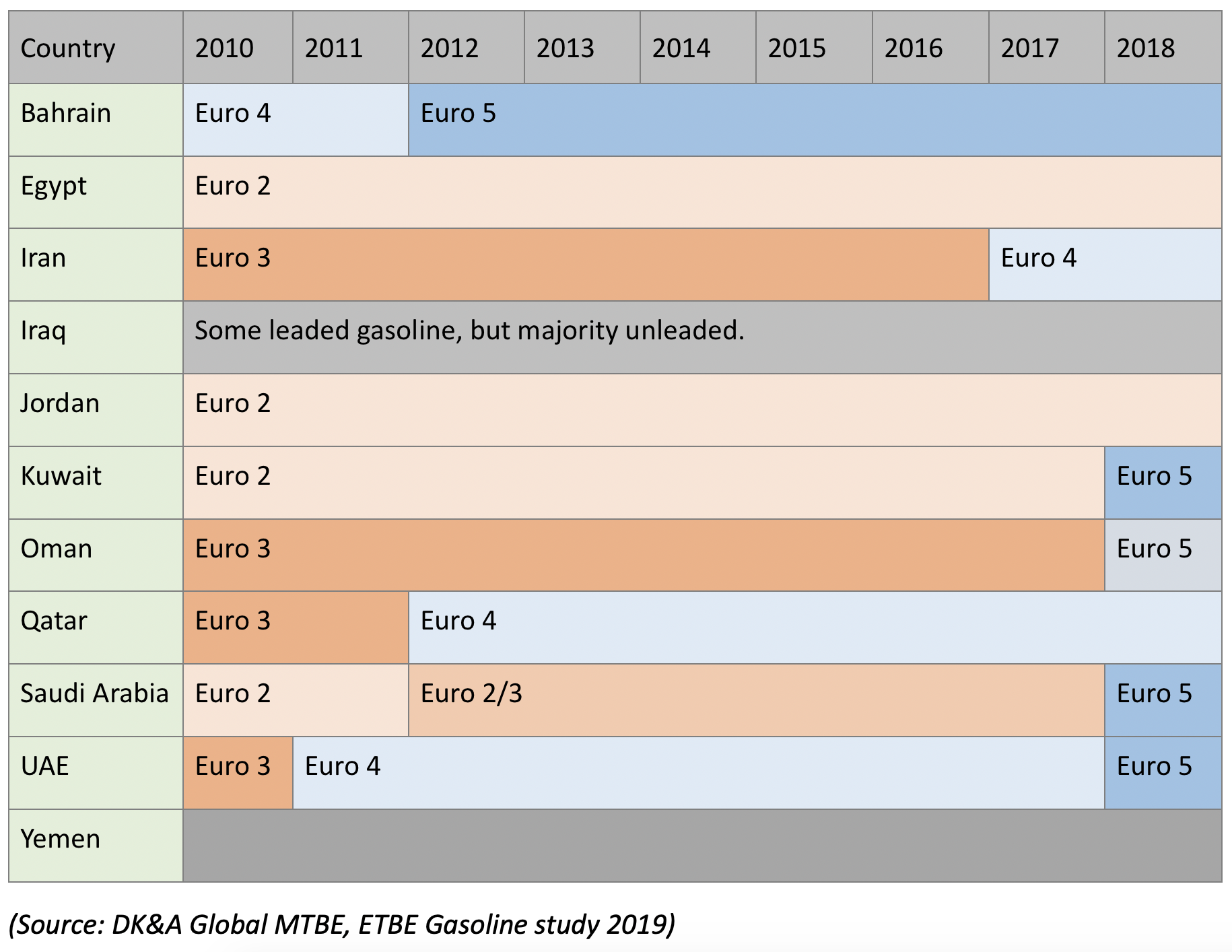

The other region which requires some specific attention is the Middle East. Over the last 10 years fuel standards in the Middle East have improved tremendously, and by today some countries have already adapted to Euro V gasoline standards and also successfully launched 95RON premium gasoline grades. However, the positive development spin focuses on some countries only while large parts of the Middle East are still trailing far behind international standards, even using leaded gasoline in some specific instances.

Gasoline consumption in the Middle East has also grown steeply since 2010, well exceeding global fuel demand increases and with the growth in affluence fuel quality requirements started changing in some parts of the Middle East accordingly. Over the last five years a long list of local refining projects, including overhauls and capacity increases of existing units, have been announced which signals that the region will over time become less dependent on transportation fuel supplies from the international market. In terms of volume as well as quality (=octane) requirements.

Besides Saudi Arabia which is with over 30% of the total Middle East gasoline consumption the biggest economy in the region, Bahrain, Kuwait, Israel, the United Arab Emirates and Oman are the countries which offer Premium gasoline grades, according to Euro V standards, while Iran also markets 95RON gasoline, albeit emission standards are still based on Euro IV. According to some consultancy reports, Premium Unleaded in Saudi Arabia today has a market share of approximately 30%, with 91RON representing the rest. This ratio we see changing over the next five to ten years to a 40:60 split, while overall gasoline demand will grow from an estimated 28m MT/y currently to about 36m MT/y over the next decade. In Iran, the regions 2nd largest economy, overall gasoline consumption represents about 22.5% of the Middle East total. The current gasoline octane split between Regular and Premium is >90/ <10 and this likely to change to a 80/20-ratio over time, while the overall gasoline market will grow, from 21m MT to about 27m by 2030.

Overall, the above-mentioned countries represent about 70% of the total gasoline demand in the Middle East, which leaves a 2nd group of countries, namely Jordan, Lebanon, Egypt, Qatar and Syria, with typical Euro III/IV standards and a range of various octane requirements with a market share of 20%, and a 3rd group with low standards/low octane ratings behind. The 3rd category of countries (Iraq, Yemen, others) represents <10% of the overall gasoline market in the Middle East.

The table underneath gives the reader some focus as to what the current fuel specification targets in the Middle East are, clearly indicating that this region is far from a harmonized, uniform standard, leaving the countries in a very fragmented environment.

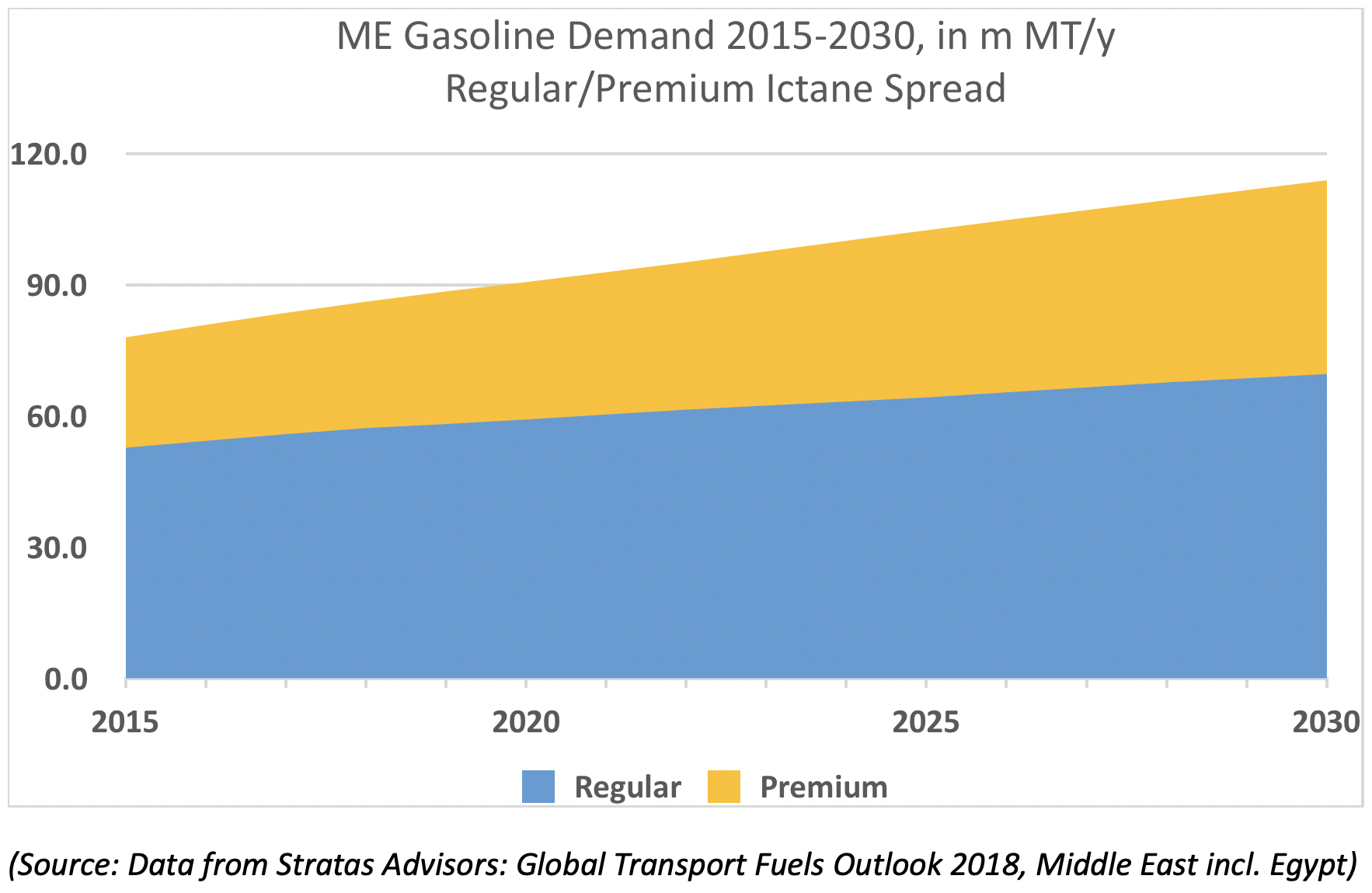

Having said this, this also represents a significant chance for octane growth, as the overall objective can only be to raise standards in lower quality countries to the to-date established, highest octane qualities. However, this has been identified as the major challenge in the Middle East as till date initiatives to harmonize fuel standards have failed to materialize region-wide and advocates in this market segment will be required to maintain a high level of pressure on local policy makers and authorities. The chart below shows how the overall gasoline demand is projected to grow between now and 2030 and how the split between Regular and Premium gasoline will unfold, basis the given fuel specification requirements in the countries.

According to Stratas, gasoline demand in the Middle East will grow by over 30% between now and 2030, and the octane split between Regular and Premium gasoline will change, from currently just under 70:30 to about 60:40 during the same time frame, based on today’s known and announced gasoline specification modifications.

Africa

The continent is often forgotten about when it comes down to global fuel demand and quality changes. However, Africa shows some significant growth potential, for both volume and quality. Today, largely a low-octane/low quality market, Africa is already an important destination for fuel supplies ex Europe, the Middle East and even South-East Asia, importing in total about 24m MT/y, as the continent’s oil industry is underdeveloped and in urgent need of modernization. The Import total equates to about 50% of Africa’s current gasoline demand, meaning that only 50% of the continent’s total consumption is locally produced.

While Africa remains a difficult region to predict accurately into the future, as far as quality and octane requirements are concerned, the fact that gasoline consumption is expected to grow by almost 30%, from 47.2m MT to 61m MT by 2030, is a good indication that the continent’s octane demand will also grow in the years to come, particularly as quality standards today are far behind international standards.

Overall, ACFA sees an enormous potential for octane growth, mainly coming from fuel quality and octane improvements in South-East Asia, the Middle East and Africa, while China, the world’s 2nd largest consumer of gasoline and a front-runner in terms of quality standards, also provides plenty of space for improvements, in terms of lifting octane requirements. Latin America will need to find a balance between fuel quality and octane requirements, the cost of implementing any changes for the supply industry as well as for the consumer versus the currently available local supply and the impact of the extra outflow of foreign exchange on each state’s budget.

Developments for specific high-octane fuels, like SuperPlus and other >100 RON fuels, although environmentally beneficial and requested by the automotive industry, will need additional public support, from consumers, legislators and other stakeholders in order to break out of their niche market position, as they will lack the support of the oil industry.

In this issue of our “In Conversation with” we talked to Mr. Jeff Hove, acting Vice President and Executive Director at the Fuels Institute. In recent years we have seen some initiatives to consider policies to ban the sale of vehicles equipped with internal combustion engines (ICE), predominantly emerging in Europe, but also spreading out in parts of Asia.

In this issue of our “In Conversation with” we talked to Dr Tilak Doshi, an energy sector consultant based in Singapore. Dr Doshi shared his views and observations about the global “2050 decarbonisation” plan and move towards Electric Vehicles (EVs) with us. We would like to thank Dr Doshi for his efforts to comprehensively answer our questions which provide some highly valuable and very interesting insights into this matter, highlighting a range of topics often overlooked in the political discussion between the various stakeholders in the race to save the world from impending climate catastrophe.

In this issue of our “In Conversation with” we talked to Dr Sanjay C Kuttan, Chairman of the Sustainable Infrastructure Committee at Sustainable Energy Association of Singapore (SEAS).

.svg)

.svg)